Life Insurance, Learn the Plans

So you know you need Life Insurance, we all do. But how do you choose the best plan for you? We can help you evaluate the needs and goals for you and your family and guide you to the best policy to provide you with real comfort and security. Learn more here, or click below to get rates from our A+ rated carriers!

Get CoveredOptions to meet any Goal!

Whole Life Insurance

Final Expense

Final Expense- Instant Approval

- Cash Value

- From $5,000 to $2,000,000

- Living Benefits

Universal Life Insurance

Permanent coverage with flexible premiums. Option to guarantee death benefit. Ability to borrow against your policy. Instant Approval.

Term Life Insurance

Choose the term that works for you; 10-, 15-, 20-, and 30-year terms available in addition to permanent products. Whatever your needs, we have it covered.

Fast, online life insurance with no medical exam

Complete our 100% online application in minutes. Just answer a few health questions and receive your life insurance quote today with no requirements of a medical exam.

APPLY NOWWhole Life & Final Expense

What is whole life insurance?

Whole life insurance can last the rest of your life with a guaranteed payout for your loved ones.

Whole life insurance may be a great fit for you if:

- You want coverage for the rest of your life

- You want a policy to build cash value over time

- You want to invest for a long-term benefit

Our whole life insurance for seniors

We’re striving to make getting whole life insurance simpler, faster, and just plain easier here. AtmosLife can help you find whole life insurance with guaranteed approval in a matter of minutes for those ages 60 to 85, no matter your health history. With no medical exams, simply answer a few health questions to help determine the rate on your guaranteed coverage. Policies range from $1,000 to $50,000 and feature a secure rate that never increases, covering you for life.

I Need This

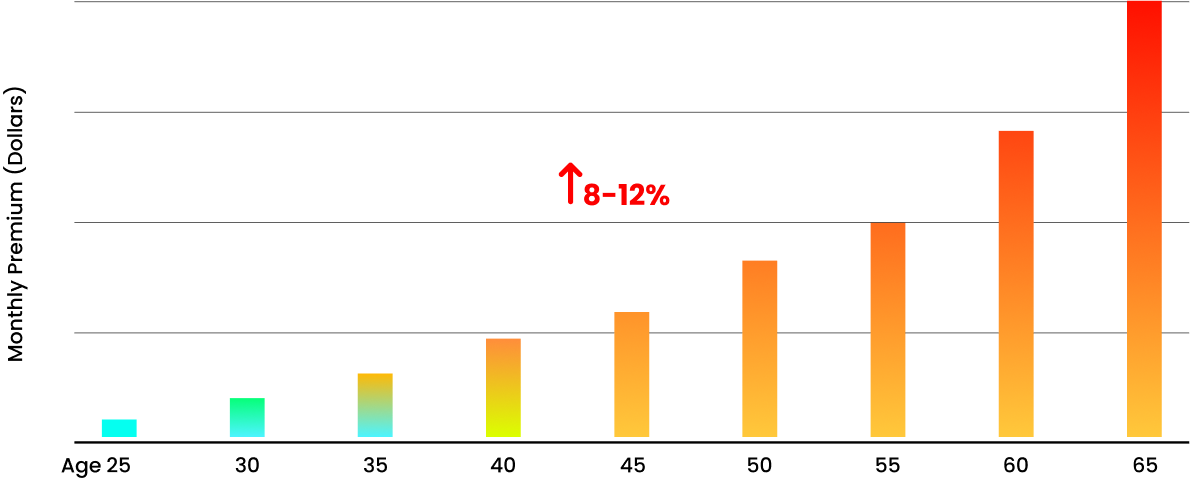

Rates by AGE - this goes up, every year you wait...

Indexed Universal Life

What Is Indexed Universal Life (IUL) Insurance?

Indexed Universal life (IUL) insurance is a type of permanent life insurance that, like other permanent insurance, has a cash value element and offers lifetime coverage as long as you pay your premiums. Unlike whole life insurance, universal life allows you to raise or lower your premiums within certain limits, and it can be cheaper than whole life coverage. Great for mid 40’s with family and even up to 75 years old!

As the name implies, the COI is the minimum amount of a premium payment required to keep the policy active. It consists of several items rolled together into one payment. COI includes the charges for mortality, policy administration, and other directly associated expenses to keep the life insurance policy in force. If you are generally healthy, this is the way to go!

THE Alternative to Final Expense if you’re 60+

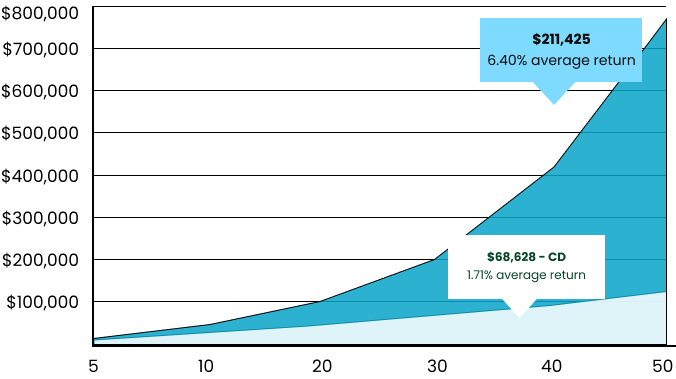

Rates for IULIUL CASH VALUE EXAMPLE

IUL policies typically allow you to grow a portion of your premiums through allocation to an index. Insurers often offer a growth cap of 8-9% and floor of 0%. This allows for upside potential with downside protection. Did I mention it’s all tax-efficient?

Get a Rate!

DEATH BENEFIT

A death benefit will be associated with the policy based on an individual's age and health.

- Example of an IUL policy that achieves a 6.4% annual return with tax deferral and reinvested dividends*

- Bank Savings CD account averages 1.71% annual return with taxable interest payments at 35%*

*Tables and charts are for illustrative purposes only and are not based on any specific policy example. Please reference your specific policy for additional details. All guarantees and contractual obligations are based solely on the claims-paying ability of the issuing life insurance company.

“I have been working with this company for several years. I have always been very happy with them. Check them out!”

Barb W.

“When I needed to get life insurance for my mother, I ended up also getting it for myself too....was blown away with the accuracy, details, and knowledge I got from them.”

Derek B

“Have looked at life insurance for a while now and, since I am 68 years old, was frustrated but they got me what I need, great rate, great people.”

James R.

“No pressure, no calls all the time, and I found a plan I didn’t even no existed, was approved that day. My husband too. Easy to deal with and knowledgeable.”

Wendy D.

“I have an awesome Agent....Provides great, timely, responsive communicative service, available by phone, text or email.”

Elizabeth F.

Term Life Insurance

What is it and how does it work?

Term life insurance features the most straightforward and affordable life insurance option by covering you for a set "term" (typically 10 to 30 years). If you pass away during the term period, your beneficiaries receive a cash payment.

Term life insurance with atmos might be right for you if:

- Your loved ones would need to replace lost income while raising children or paying a mortgage (also called Mortgage Insurance)

- You have short-term financial responsibilities such as loans, a new business, or credit card debt

- You want the most affordable life insurance coverage

- You appreciate the straightforward nature of term life insurance

We have VERY unique plans, even TERM plans that don’t run out! What does this mean? It means, if your term policy runs out, you can keep it and still pay the same amount, but with a reduced benefit, so you don’t end up with no coverage!

See your Rates

How to expedite your application

When you apply, answer each question with as much detail and accuracy as possible. And be sure to have the following information handy

If you’re asked to answer any follow-up questions, be sure to take care of these requests as soon as possible. The policy underwriting process will be delayed until these steps get completed.

Common mistakes when buying life insurance

Waiting until you have kids

If you delay buying life insurance until you have kids, it could cost you valuable years of locking in a low premium. Even if you don't yet have children to protect, life insurance can cover your personal debts,medical bills, home mortgage, lost wages, and even funeral expenses.

Your health status is one of the most crucial factors when determining premiums. The healthier you are, the less you pay, so getting life insurance at a younger age can be advantageous. As you age, the risk of developing health issues (such as cancer or diabetes) can lead to higher premiums and sometimes make it difficult to get coverage. Securing life insurance earlier in life helps protect you— and those who depend on you—against any unexpected changes.

Relying on employer-sponsored coverage

Employer-provided life insurance is a nice benefit, but these policies rarely offer sufficient coverage. Employer-sponsored policies typically only provide coverage of one to two times your annual salary.However, financial experts recommend you carry coverage about ten times your salary. And any change to your employment status (such as retirement, layoff,or job change) likely means you’ll lose the policy. If a change occurs when you're older—or after you've developed a health issue—it could be more expensive and difficult to secure new coverage. Having your own policy helps protect you and your loved ones against life’s unexpected changes.